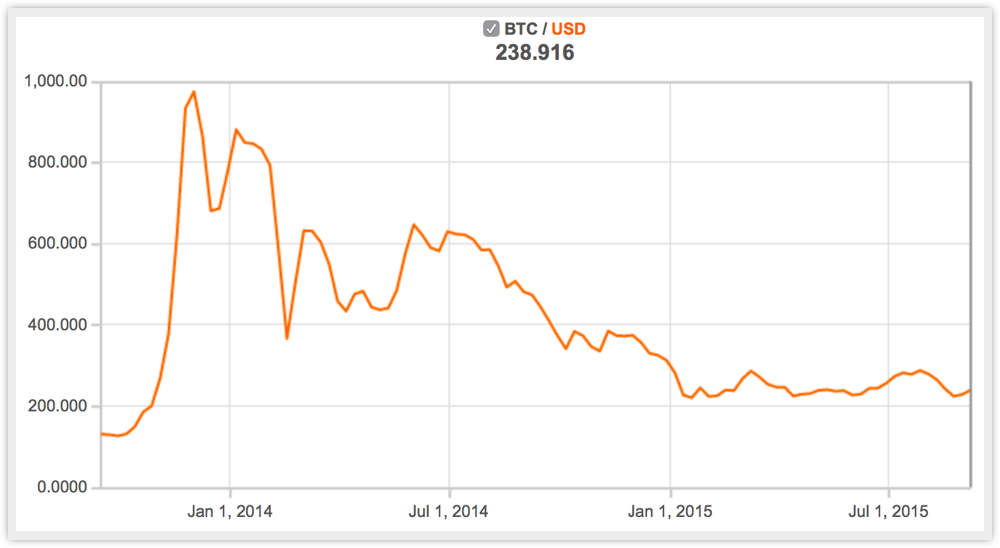

– Approximate Bitcoin-to-US$ rate (from oanda.com) –

Mt. Gox was once the world’s biggest Bitcoin exchange.

Now it’s a heap of digital rubble, after collapsing in early 2014.

The company filed for bankruptcy after admitting it had “lost” customers’ bitcoins that were worth about $500,000,000 at the time.

“Losing” bitcoins isn’t like a regular bank getting your balance wrong, or approving a fraudulent transaction out of your account, where there is at least a chance of reversing the mistake and recovering some or all of your missing funds.

When a crook makes off with stored bitcoins, that’s like armed robbers hitting a security van and making off with bags and bags of cold, hard cash.

With no central control over the ecosystem, a very short history, and almost no global regulation, it’s not easy to decide whether a Bitcoin exchange is trustworthy or not.

Indeed, you have to trust the staff at your chosen exchange to do two things: firstly, not to store your bitcoins where they can be reached and pilfered by hackers; and secondly, not to blame hackers and run off with your bitcoins themselves.

If either of those things happens, it can be tricky to work out which one it was.

The Mt. Gox story

That’s where we are with Mt. Gox.

That’s where we are with Mt. Gox.

Mark Karpeles, Mt. Gox’s founder, has understandably denied any direct involvement in the vanishing Bitcoinage.

But at the very start of 2015, a Japanese newspaper openly stated that there was “strong suspicion” that most of the missing Bitcoins were ripped off from inside Mt. Gox.

650,000 bitcoins had gone missing; Yomiuri Shimbun claimed that only about 7000 of those could be explained away by cyberattack – in other words, by the machinations of crooks outside Mt. Gox’s network.

According to Yomiuri Shimbun, the disappearance of the other BTC643,000 – 99% of the vanished funds – was down to an inside job.

Despite this claim, Karpeles was arrested at the start of August on charges relating to overstating his financial position.

If true, that would have been unfair to investors and customers, not to mention illegal, but it wouldn’t have explained any of the missing bitcoins.

Now, apparently, Karpeles is deeper in, arrested a second time and charged with what numerous reports describe as “embezzlement.”

If true, that’s a bit more serious than pretending you’re in a stronger financial position than you really are.

Embezzlement would mean that Karpeles withdrew money from the company – money invested by his customers – and took it for himself.

It’s still not the same as directly stealing bitcoins, but it’s bad news for Karpeles.

What about the missing bitcoins?

Reports suggest that the amount involved is ¥341,000,000, which works out to about $2.8m.

That’s not good news for the investors who lost money on Mt. Gox.

Bitcoins are down substantially from their heyday before Mt. Gox’s collapse, when they flirted with a value of $1000 each.

But even at BTC1 = US$240, the approximate rate at the time of writing, $2.8m is a tiny fraction of the value of the missing bitcoins, which remain, as ever, missing.

Anonymous

Wasn’t bitcoin special in that no two coins are alike, if you have the # of your coin it should be detectable in transaction, 100% not anonyms as in what coin is used. For that matter, if there was a real bitcoin bank, you should be able to see the location of every coin at any time. Or it’s was a scam in the first place. :)

Bill

After thuis incident the IMF should declare that the Bitcoin existance is illegale and is a criminal valuta. All the riscs of losing value is for the owner and trading in Bitcoins should become illegale and criminal.

Stampy

Actually three things. The third is in the name “Exchange”. Why oh why would you exchange your hard earned cash for bitcoins and then LEAVE it all there? You can EASILY transfer your bitcoins back to your personal wallet. In fact that is the whole point of the Bitcoin protocol, you ARE your own Bank! The ONLY reason you would leave your bitcoins “on the web” in an Exchange is so you can do instant speculative trading on the $1000 per Bitcoin hype that was causing a Trader feeding frenzy around then, OR for trading anonymously on the Dark Web in “illegal” places like Silk Road……

Again, at that time, Bitcoin was strictly for the Geeks, Traders and Dark Web folk. Your average Jo certainly would have put more than a few bucks into bitcoins to play around a bit, there wasn’t even much you could “buy” with bitcoins at the time even if you wanted to! (Apart from drugs, explosives and poisons on the Dark Net!)

So I believe MOST of those who lost money were speculative traders (many of whom may have purchased bitcoins at $20 a year before) and the “losses” were actually technical (grossly inflated Bitcoin price).

I suspect the rest were Dark Net traders, who must indeed be pretty unhappy about their losses, and Mr Mark Karpeles, what-ever the outcome of the Judicial processes in Japan, probably shouldn’t bother wasting his money on long term retirement and pension plans … :-(

Stampy

To Anonymous: LoL! The satoshi is currently the smallest unit of the bitcoin currency recorded on the block chain.It is a one hundred millionth of a single bitcoin (0.00000001 BTC). Each satoshi of each bitcoin can be spent separately. So a stolen bitcoin can be mixed (Tumbler) with other (clean) bitcoins making direct tracing hard, if not impossible, since all wallets and Exchange Accounts can also be (almost) anonymous. No, it’s not a scam, it’s COIP (Currency over IP). It’s ever increasing adoption clearly means the Financial world are taking notice of the Bitcoin Protocol and the Blockchain and adopting it.

To Bill: The IMF has no regulatory powers, only advisory. Some governments have made bicoin illegal, interestingly the only ones so far are the most corrupt countries on earth! Making bitcoin illegal would require making all Virtual Currency illegal, and that would also catch Store loyalty cards, Amazon coins, and many other similar virtual currency things.You could argue that fiat (currency) is Virtual since only 5% exists as coins and notes, the rest, like bitcoins are just numbers on a computer disk, and unlike bitcoin even down to satoshi level, the stored fiat does not have unique identifiers, so far more risky for use in fraud situations and totally untraceable, unlike bitcoins.

Coins and notes are also untraceable iun a provable sense legally. Bitcoin down to satoshi is fully traceable.

As a comment 75% of banknotes in circulation have traces of cocaine on them. The worlds drug trade is based on the US dollar. So logically in priority order, you would ban US dollars as the principal funding of the drug trade, before banning bitcoin for just having the same potential..

Some would argue that the folks in Finance who “lost/stole/mislaid” several trillion dollars in the financial crash would better fit your description of criminal, however only a couple have even been charged with any crime.

Bitcoin is simply the next step in computerisation, in this case of money. Trying to stop it will be as successful as the Luddites and Victorian machine breakers, you have to adapt to IT progress, you certainly won’t stop it.

Anonymous

I’ve seen that statistic “X% of banknotes in circulation have traces of Y on them” many times, for many values of Y. (You also used to hear it in the form “M% of peppermints in the help-yourself jar where you pay your bill in a restaurant have traces of N on them,” for some rather eye-openingly unhygienic values of N. Those claims have died out since the advent of the individually-wrapped restaurant departure sweet.)

There must be a whole raft of banknote analysts in every country of the world doing an awful lot of fairly pointless but meticulous (and very sensitive) assay work.

I wonder who funds them, and why?

Andrew Ludgate

Bitcoins themselves have a block chain, which means you can trace them back through their transactions.

But in this case, Mt. Gox was an exchange, where you could launder your cash/bitcoins for bitcoins/cash — meaning that the chain is broken.

From a customer side, they’d have a blockchain that terminated at Mt. Gox. If an insider than converted that coin over to cash held locally and traded the coin back out to someone else, that’s totally legitimate (it’s how banks work too). But if the cash they paid out/borrwed didn’t match up against the number of coins they’d taken in and the amount they reportedly already had in escrow, there’s no way to trace those other coins, neither the imaginary ones nor the real ones for which you don’t have a block fragment to match against.

So if an insider sold off all the bitcoins that were coming in but didn’t keep the other currency in Mt. Gox’s name (but instead transferred it to private accounts), there’s nothing to connect the two sets of currency other than Mt. Gox’s bookkeeping — which appears to be where the problems are.

Stampy

Wow, Andrew! That’s an amazing four paragraphs! I couldn’t locate a single true, accurate or correct statement in any of them. May I humbly suggest you first of all read your subject, even a quick glance would be better than the meaningless confused jumble of words published above.

I would be more than happy to explain to you how the Blockchain protocols works, how the Bitcoin protocol fits onto the blockchain; why Mt Gox collapsed, how bitcoins are indeed fully traceable (on the blockchain ledger) but since the originating wallets are usually anonymous, traceable back to who?

The latest analysis of the Mt Gox fiasco shows that only a small percentage of the stolen coins actually left the Exchange. This suggests the rest are still there, hidden away, possibly. Or converted to paper wallets and hidden in the insiders secret place/s. Or simply those wallets and private keys were accidentally deleted and now lost for ever. We know all the bitcoin IDs, but without those missing private wallet keys, the coins remain tantalizingly visible on the blockchain, but without the private keys to the wallets that now contain them, they remain out of reach and unspent, so far and possibly lost for ever…..

Paul Ducklin

You say that only a small percentage of the stolen coins actually left the Exchange. Then you say that perhaps insiders stole the coins by converting them into paper wallets that they took for themselves.

In what way can both those things be true? (Unless you mean that the unlawfully-acquired paper wallets were actually physically hidden away inside Mt. Gox’s offices, which is not quite the same as “not leaving the Exchange.”)

Or are you just simply making the point that the missing bitcoins haven’t shown up back in the ecosystem yet and may never do so?

Stampy

With Virtual Currency the definition of “theft” is kinda tricky, since the coins don’t physically exist (they are mere cyphers) and anyway they haven’t moved, ie been “spent”!

Yes, I was making the point that the missing bitcoins haven’t shown up coming BACK in the ecosystem ie being SPENT yet and indeed may never do so.

However, unlike “real” money (ignoring the virtual fiat on Bank’s disks) a bitcoin can be spent by ANYONE who has the private key for the wallet that currently contains them, from ANYWHERE in the world. Mt Gox being down or it’s data is irrelevant to the bitcoins being spent.

So if multiple people all possess the private key/s to the wallet/s containing the “stolen” bitcoins, eg on a bit of paper, photocopied or memorised, but no-one attempts to actually USE/SPEND those bitcoins, are they stolen and are the key holders all thieves, or just the one who tries to spend them?

To “Stolen”, I would say legally Yes, because the original rightful owner has been “deprived of their property”,

To “thieves” I would suggest that unless it can be legally proved that one/all of them actually “moved” the coins to another wallet (to which the original owner no longer has access), there is no legal proof of theft.

If it can be legally proved that one or more people are holding the private keys to the wallet containing the “stolen” bitcoins, I guess the charge would be receiving and holding stolen property.

I also wonder if the bitcoins are legally “stolen” if they haven’t been “spent”? We can still “see” them on the Blockchain! It’s like seeing your stolen gold bars but not having the key to the cupboard, and the gold bars are still in the same cupboard (blockchain)! it’s just that the lock has been changed! Fascinating legal issue that has only arisen because of the open blockchain ledger that bitcoin rides on.

Comments?

stan

bitcoin always looked like a Ponzi scheme to me